Time Series Analysis of Nigeria External (Foreign) Reserves

Keywords:

External Reserve, Augmented Dickey-Fuller, Unit Root, StationarityAbstract

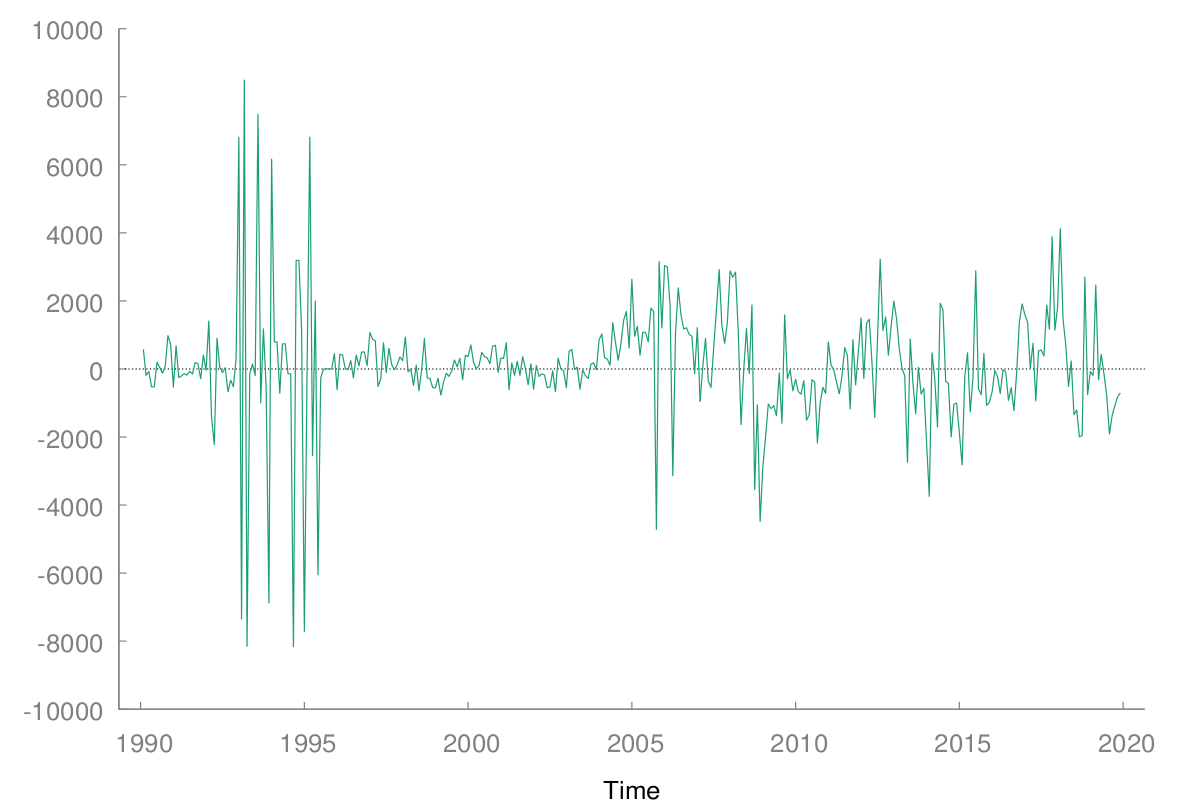

Economy of a country can absorb shock and as well boost confidence through external reserves. Hence, external reserves play an important role to the extent that it helps in stabilizing the country’s economy. This study focuses on modeling the Nigeria external reserves using time series technique. 30-year data were extracted from the Central Bank of Nigeria (CBN) bulletin from 1990 – 2019. Some economic tools used to diagonize the data are Augmented Dickey Fuller (ADF) test, unit root tests Kwaitkowshi – philips – Schmiot – Shin test in order to ascertain the stationary of the data. Meanwhile, Auto Regression Integrated Moving Average (ARIMA) model was used as model for prediction whereby Akaike Information Criterion (AIC) and Hannan-Quinn Information Criterion (HQIC) were used as model diagnostic checking. At original level, the data showed an upward trend and found out to be non-stationary. When further examined using the diagnostic economic tools, at first difference the data were found to maintain a state of equilibrium. Also, model diagnostic checking revealed that ARIMA (2,1,7) was found to be the appropriate optimal model and thereby used for forecast for the next five years. Hence, the forecasted values revealed that the Nigeria external reserves will continue to increase steadily. Consequently, government should put in place legal policies that will enhance, increase accumulation and proper management of external reserves.

Published

How to Cite

Issue

Section

Copyright (c) 2023 T. J. Adejumo, A. I. Okegbade, J. I. Idowu, O. J. Oladapo, O. O. Oladejo

This work is licensed under a Creative Commons Attribution 4.0 International License.

How to Cite

Similar Articles

- Ahmad M. Shuaibu, Kizito O. Musa, Ijioma M. Okiyi, Groundwater recharge modelling using SWAT analysis for groundwater reserve quantification of Ka watershed catchment area part of Sokoto-Rima Basin, North West Nigeria , African Scientific Reports: Volume 4, Issue 1, April 2025

- E. A. Yerima, A. U. Itodo, R. Sha’Atob, R. A. Wuana, G. O. Egah, S. P. Ma’ajia, Phytoremediation and Bioconcentration of Mineral and Heavy metals in Zea mays Inter-planted with Striga hermonthica in Soils from Mechanic Village Wukari , African Scientific Reports: Volume 1, Issue 2, August 2022

- Emmanuel Joseph, Gonto Kamal, Oluwasesan M. Bello, Natural radionuclide distribution and analysis of associated radiological concerns in rock samples from a rocky town (Dutsin-Ma) in the North-Western region of Nigeria , African Scientific Reports: Volume 2, Issue 3, December 2023

- Justine Utsu Undiandeye, Moses Adah Agana, Towards strengthening edge computing security through stack protection mechanisms , African Scientific Reports: Volume 5, Issue 2, August 2026

- Otor Daniel Abi, Anene Gerald Makuachukwu, Daniel Ominyi Sunday, Peter Ikpe Adoga, Ortwer Felix Igbasue, Numerical evaluation of energy shifts due to dipole moments interaction in a hydrogen atom , African Scientific Reports: Volume 5, Issue 1, April 2026

- E. A. Oni, C. O. Ajiboye, P. S. Ayanlola, O. O. Oloyede, A. A. Aremu, T. A. Olajide, O. O. Oladapo, O. P. Oyero, A. E. Oladipo, M. K. Lawal, Measurement and simulation of indoor radon concentration distribution in students’ residential hostels around Ladoke Akintola University of Technology, Ogbomoso, Nigeria , African Scientific Reports: Volume 4, Issue 3, December 2025

- I. M. Echi, E. V. Tikyaa, E. J. Eweh, A. A. Tyovenda, T. Igbawua, Investigation of the spatial distribution of deterministic chaos in some meteorological variables across Nigeria , African Scientific Reports: Volume 4, Issue 2, August 2025

- Solomon Denen Igba, Idugba Mathias Echi, Emmanuel Vezua Tikyaa, Simulation of thermochemical effects on unsteady magneto hydrodynamics fluids flow in two dimensional nonlinear permeable media , African Scientific Reports: Volume 3, Issue 3, December 2024

- Chiagoziem Wisdom Chidiebere, Ugochukwu Aniefuna Azuka Anthonia, Natural Skin Whitening Compounds: Types, Source and Mechanism of Action: A Review , African Scientific Reports: Volume 2, Issue 1, April 2023

- Peace P. Desben, Emmanuel N. Dashe, Joel N. Ndam, Transmission dynamics of community-and hospital-acquired infections: insights from mathematical modelling , African Scientific Reports: Volume 5, Issue 2, August 2026

You may also start an advanced similarity search for this article.

Most read articles by the same author(s)

- Taiwo J. Adejumo, Kayode Ayinde, Abayomi A. Akomolafe, Olusola S. Makinde, Adegoke S. Ajiboye, Robust-M new two-parameter estimator for linear regression models: Simulations and applications , African Scientific Reports: Volume 2, Issue 3, December 2023

- Janet Iyabo Idowu, Olasunkanmi James Oladapo, Abiola Timothy Owolabi, Kayode Ayinde, On the biased Two-Parameter Estimator to Combat Multicollinearity in Linear Regression Model , African Scientific Reports: Volume 1, Issue 3, December 2022