Time Series Analysis of Nigeria External (Foreign) Reserves

Keywords:

External Reserve, Augmented Dickey-Fuller, Unit Root, StationarityAbstract

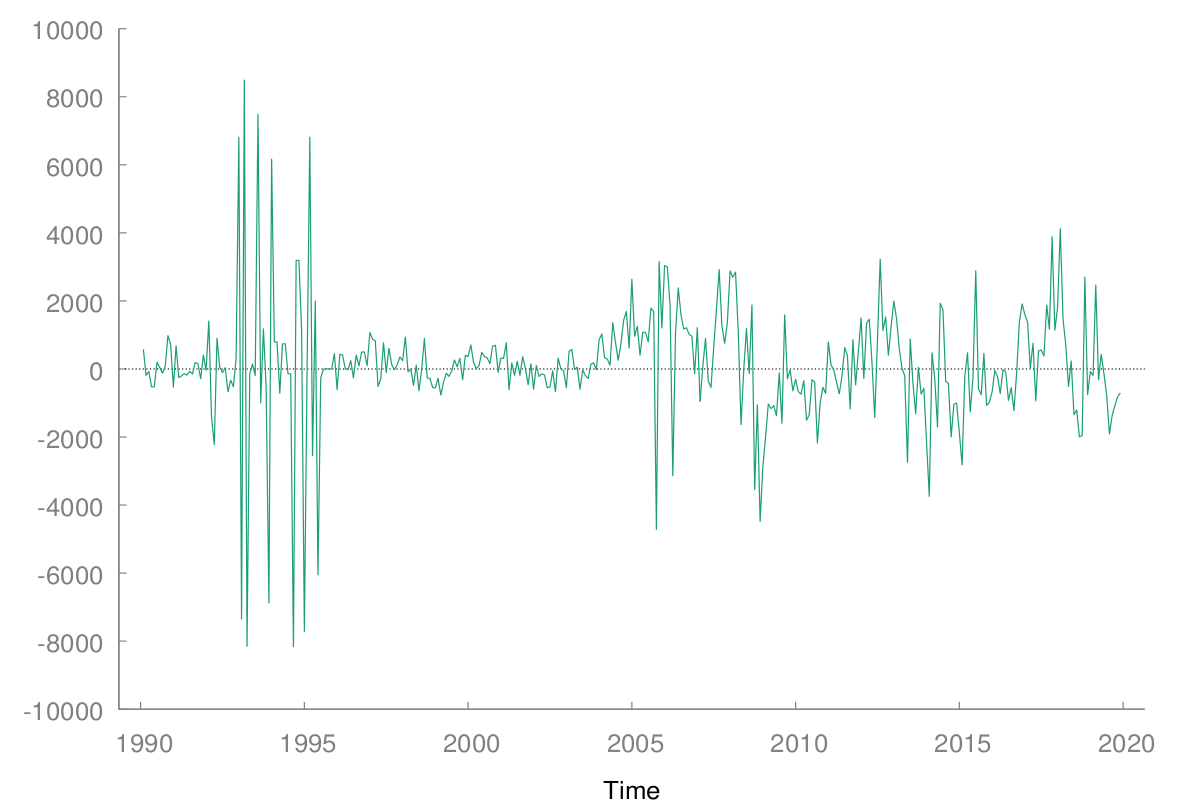

Economy of a country can absorb shock and as well boost confidence through external reserves. Hence, external reserves play an important role to the extent that it helps in stabilizing the country’s economy. This study focuses on modeling the Nigeria external reserves using time series technique. 30-year data were extracted from the Central Bank of Nigeria (CBN) bulletin from 1990 – 2019. Some economic tools used to diagonize the data are Augmented Dickey Fuller (ADF) test, unit root tests Kwaitkowshi – philips – Schmiot – Shin test in order to ascertain the stationary of the data. Meanwhile, Auto Regression Integrated Moving Average (ARIMA) model was used as model for prediction whereby Akaike Information Criterion (AIC) and Hannan-Quinn Information Criterion (HQIC) were used as model diagnostic checking. At original level, the data showed an upward trend and found out to be non-stationary. When further examined using the diagnostic economic tools, at first difference the data were found to maintain a state of equilibrium. Also, model diagnostic checking revealed that ARIMA (2,1,7) was found to be the appropriate optimal model and thereby used for forecast for the next five years. Hence, the forecasted values revealed that the Nigeria external reserves will continue to increase steadily. Consequently, government should put in place legal policies that will enhance, increase accumulation and proper management of external reserves.

Published

How to Cite

Issue

Section

Copyright (c) 2023 T. J. Adejumo, A. I. Okegbade, J. I. Idowu, O. J. Oladapo, O. O. Oladejo

This work is licensed under a Creative Commons Attribution 4.0 International License.